UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report

(Date of earliest event reported):

(Exact name of Registrant as specified in its charter)

(State of Incorporation) |

(Commission File Number) |

(I.R.S. Employer Identification No.) |

| (Address of principal executive offices) | (Zip Code) |

(

(Registrant’s telephone number, including area code)

(Former Name or Former Address, if Changed Since Last Report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the Registrant under any of the following provisions:

| Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) | |

| Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) | |

| Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) | |

| Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) |

Name of each exchange on which registered | ||

Indicate by check mark whether the Registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (17 CFR §230.405) or Rule 12b-2 of the Securities Exchange Act of 1934 (17 CFR §240.12b-2).

Emerging growth

company

If an emerging growth company, indicate

by check mark if the Registrant has elected not to use the extended transition period for complying with any new or revised financial

accounting standards provided pursuant to Section 13(a) of the Exchange Act.

| Item 7.01 | Regulation FD Disclosure. |

Sun Country Airlines Holdings, Inc. intends to conduct an investor presentation beginning on June 23, 2022. A copy of the investor presentation is attached hereto as Exhibit 99.1 and incorporated by reference herein.

The information contained in this report, including Exhibit 99.1 attached hereto, shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities of that section, nor shall it be deemed incorporated by reference in any filing under the Securities Act of 1933, as amended, or the Exchange Act, regardless of any general incorporation language in such filings, unless expressly incorporated by specific reference in such filing.

| Item 9.01 | Financial Statements and Exhibits. |

(d) Exhibits.

| Exhibit No. | Description | |

| 99.1 | Presentation dated June 2022 | |

| 104 | Cover Page Interactive Data File (embedded within the Inline XBRL document) |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, as amended, the registrant has duly caused this report to be signed on its behalf by the undersigned thereunto duly authorized.

Date: June 22, 2022 |

Sun Country Airlines Holdings, Inc. |

|||

| By: | /s/ Eric Levenhagen | |||

| Eric Levenhagen | ||||

| Chief Administrative Officer, General Counsel and Secretary | ||||

EXHIBIT 99.1

Sun Country Airlines June 2022

Disclaimer This presentation has been prepared by the Company for informational purposes only and not for any other purpose. Nothing con tai ned in this presentation is, or should be construed as, a recommendation, promise or representation by the presenter or the Company or any director, emplo yee , agent, or adviser of or the Company. This presentation does not purport to be all - inclusive or to contain all of the information you may desire. Market Data We include statements and information in this presentation concerning our industry ranking and the markets in which we operat e, including our general expectations and market opportunity, which are based on information from independent industry organizations and other third - part y sources (including a third - party market study, industry publications, surveys and forecasts). While we believe these third - party sources to be reliable as of the date of this presentation, we have not independently verified any third - party information and such information is inherently imprecise. In addition, projectio ns, assumptions and estimates of the future performance of the industry in which we operate and our future performance are necessarily subject to a high degre e o f uncertainty and risk due to a variety of risks. These and other factors could cause results to differ materially from those expressed in the estimates made by the independent parties and by us. Cautionary Note Regarding Forward - Looking Statements This presentation contains forward - looking statements, which involve risks and uncertainties. These forward - looking statements a re generally identified by the use of forward - looking terminology, including the terms “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend, ” “likely,” “may,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “target,” “will,” “would” and, in each case, their negative or other va rious or comparable terminology. All statements other than statements of historical facts contained in this presentation, including financial guidance and pro jec tions and statements regarding our strategy, future operations, future financial position, future revenue, projected costs, prospects, plans, objectives of mana gem ent and general economic trends and trends in the industry and markets are forward - looking statements. These statements involve known and unknown risks, uncerta inties and other important factors that may cause our actual results, performance or achievements to be materially different from any future results, pe rfo rmance or achievements expressed or implied by the forward - looking statements. Certain of these risks are identified and discussed in our filings with the Securi ties and Exchange Commission. These forward - looking statements reflect our views with respect to future events as of the date of this presentation and are based on assumptions and subject to risks and uncertainties. Given these uncertainties, you should not place undue reliance on these forward - looking statements. We undertake no obligation to update any forward - looking statements, whether as a result of new information, future events or otherwise after the date of this presentati on. Non - GAAP Financial Measures This presentation includes certain non - GAAP financial measures, including Adjusted EBIT, Adjusted EBIT Margin, Adjusted EBITDA, Adjusted EBITDA Margin, Adjusted Operating Income, Adjusted Operating Income Margin, Adjusted Net Income, Adjusted CASM and free cash flow. These non - GAAP finan cial measures are not measures of financial performance in accordance with GAAP and may exclude items that are significant in understanding and ass ess ing our financial results. Therefore, these measures should not be considered in isolation or as an alternative or superior to GAAP measures. You shoul d b e aware that our presentation of these measures may not be comparable to similarly - titled measures used by other companies. Please see the reconciliations included in the Appendix to this presentat ion. 2

Business Overview

Differentiated and Unique Aviation Company 4 Highly Synergistic Businesses Resiliency Through the Cycle High Growth High Margin Strong Cash Flow Superior Unit Profitability Differentiated Balance Sheet Contracted Recurring Revenue Streams Sun Country was built to generate best in class performance in most environments

Uniquely Resilient Business 5 1. Comparable carriers includes Allegiant, Frontier and Spirit. • Diversified across three lines of business with strong cross utilization of pilots and aircraft • Approximately one - third of revenue comes from Cargo and Charter business featuring long - term stable contracts More Stable Earnings & Cash Flow • Charter and Cargo customers responsible for fuel costs which provides a natural hedge on approximately one - third of our usage • Q1 2022 fuel costs represent 28.5% of Sun Country’s revenue versus a 35.5% average at comparable carriers (1) Fuel Cost Pass - Through • Flexible scheduling approach targets flying at maximum unit revenue opportunities and flying is limited in “trough” periods • Low cost - mid - life fleet strategy keeps aircraft costs low Profitability Not Utilization Dependent • Well positioned to capitalize on return of vacationers and VFR passengers • Position as premier leisure carrier at MSP has allowed Sun Country to grow and attain significant market share Leisure Focus

Approximately 1/3 of fuel usage is paid for by Charter and Cargo customers Unique, Diversified Business Model 6 Sun Country Business Line Synergies Aircraft Pilots Shared Services Charter (~19% of Revenue (1) ) Passenger Leisure (~68% of Revenue (1) ) Cargo (~13% of Revenue (1) ) Standard fleet of 41 Boeing 737s that are used across scheduled service and charter; 12 737 Freighters used for Cargo 482 (2) Pilots that serve across the entire set of assets An already lean operation supporting the entire set of assets 1 2 3 • Unique low cost airline with focus on leisure travel • Flexible capacity model focused on peak demand • Greater resilience and growth opportunities than other passenger carriers • A leader in U.S. narrowbody charter • Contracted recurring revenue with pass - through costs (including fuel) • Large, stable customer base • Long - term asset - light contract with pass - through costs • High margins and cash flows • Partnership with one of the fastest growing companies globally Shared Foundational Assets 1. Percentage of total revenue as of LTM March 31, 2022. 2. As of April 30, 2022. Sun Country’s symbiotic business lines share assets to maximize operating leverage

Business Model Has Facilitated Rapid Growth… 7 Significant Growth Since 2017… …Already Exceeding 2019 Levels $559 $722 2017 LTM Q1 22 $701 $722 2019 LTM Q1 22 Our financial performance has demonstrated growth and resilience inherent in our business model (Revenue, $mm) (Revenue, $mm)

…And Outperformance in COVID and Through the Recovery 8 2020 Adj. EBIT Margin 2021 Adj. EBIT Margin Q1 2022 Adj. EBIT Margin (1) (12%) (33%) (57%) (58%) SNCY ULCCs Big Four Mid Sized Carriers 8% (9%) (10%) (13%) SNCY ULCCs Mid Sized Carriers Big Four 10% (12%) (14%) (18%) SNCY Big Four ULCCs Mid Sized Carriers Source: Public filing. Our business model results in stability through the cycle, outperforming the industry during the depths of COVID SNCY ULCCs Mid Sized Carriers Big Four

Model Generates Highest Unit Profits 9 Q1 2022 TRASM – Adj CASM (Stage Length Adjusted (1)(2) ) Source: Public filings, Diio Mi. 1. Stage length adjusted to SNCY stage length of 1,336. 2. Adj. CASM is adjusted for special items and excludes fuel. Sun Country TRASM and Adjusted CASM exclude cargo. 4.5¢ 1.8¢ 1.8¢ 1.4¢ SNCY Big Four ULCCs Mid Sized Carriers (¢) Spread between passenger unit revenue and unit cost is the best in the industry; results exclude cargo flying which further improves earnings SNCY ULCCs Mid Sized Carriers Big Four

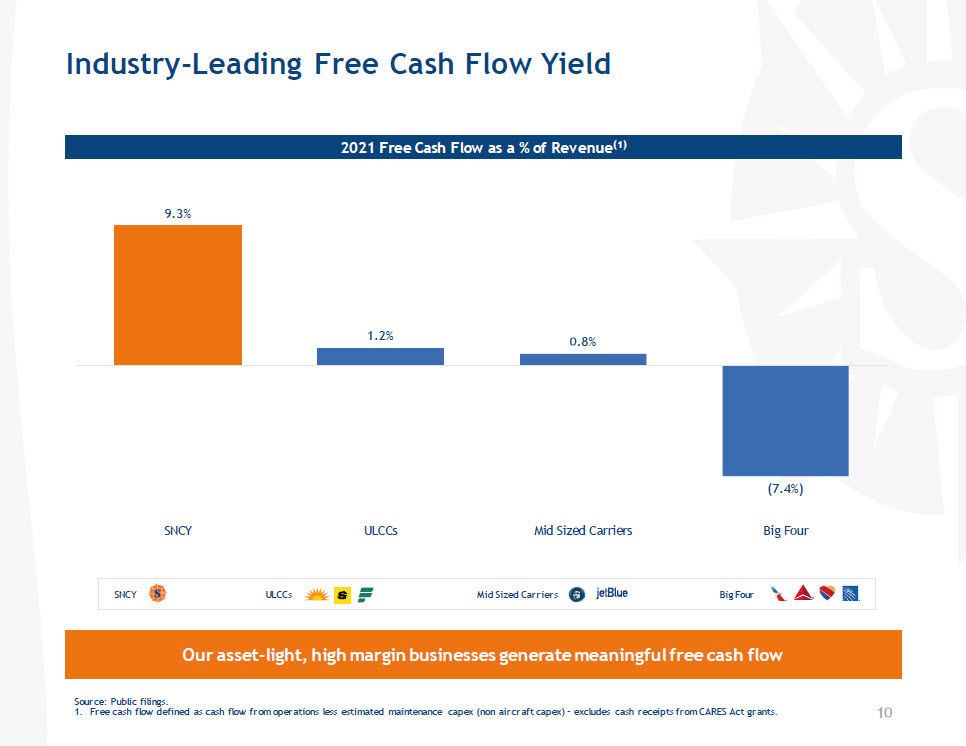

Industry - Leading Free Cash Flow Yield 10 2021 Free Cash Flow as a % of Revenue (1) Source: Public filings. 1. Free cash flow defined as cash flow from operations less estimated maintenance capex (non aircraft capex) – excludes cash receip ts from CARES Act grants. 9.3% 1.2% 0.8% (7.4%) SNCY ULCCs Mid Sized Carriers Big Four Our asset - light, high margin businesses generate meaningful free cash flow SNCY ULCCs Mid Sized Carriers Big Four

Flexible Scheduled Service Route Network 11 ~97% of our markets are seasonal which reflects demand trends of our customer

Agile Passenger Capacity Built to Capture Highest Unit Revenues 12 Seasonal Demand Dictates Monthly Schedule Day - of - Week Capacity Determined by Demand Patterns (1) Results in Higher Unit Revenue Versus High Utilization Peers 5.00¢ 6.00¢ 7.00¢ 8.00¢ 9.00¢ 25% 50% 75% 100% Mon Tue Wed Thu Fri Sat Sun % of Peak Days ASMs TRASM 50% 60% 70% 80% 90% 100% 110% 120% ULCC SAVE SNCY 9.1¢ 7.9¢ 7.7¢ (% of Peak Day ASMs) (TRASM) Monthly Seats as % of July 2021 2021 TRASM Source: Diio Mi. 1. Based on FY2021 data. (¢) Unlike other passenger airlines, we quickly shift our capacity to focus flying during peak demand to maximize our yields

Experts in Executing a Seasonal Network 13 Departures by Month at Three of Our Largest Cities MSP Departures DFW Departures LAX Departures 0 250 500 750 1,000 1,250 Jul-21 Aug-21 Sep-21 Oct-21 Nov-21 Dec-21 Jan-22 Feb-22 Mar-22 Apr-22 May-22 Jun-22 0 50 100 150 200 250 Jul-21 Aug-21 Sep-21 Oct-21 Nov-21 Dec-21 Jan-22 Feb-22 Mar-22 Apr-22 May-22 Jun-22 0 25 50 75 100 125 Jul-21 Aug-21 Sep-21 Oct-21 Nov-21 Dec-21 Jan-22 Feb-22 Mar-22 Apr-22 May-22 Jun-22 (# of Departures) (# of Departures) (# of Departures) We only fly when and where demand exists Strong North / South demand in Winter, East / West in Summer Strong summer demand to Mexico / Caribbean Strong inbound demand in Summer • RSW • MCO • PHX • CUN • LAS • LAX • SFO • LAS • SEA • ANC March 2022 July 2022 Top 5 Destinations from MSP in… 47% of Departures 34% of Departures

Unique Ability to Pass Through Fuel Costs 14 Q1 2022 Fuel Expense as a % of Revenue Q1 2022 Effective Fuel Expense per Gallon 38.1% 35.5% 32.8% 28.5% Q1 2022 Reported Fuel Price Effect of Charter Reimbursement Q1 2022 Effective Fuel Price $2.81 $3.20 ($0.39) Our unique and diversified business limits our exposure to fuel more so than peers Source: public filings. Excludes Cargo, where Amazon pays for 100% of the fuel cost

We Offer A High - Quality Product 15 Weighted Average Seat Pitch Seat Recline In - Flight Entertainment In - Seat Power Free Beverage 31” P P P P 32” P P P P 30” O O O O 30” O O O O 28” O O O O

Leader in Ancillary Revenue Generation 16 Ancillary Revenue per Passenger Growth Range (1) Benefits of Ancillary Revenue 2021 Ancillary Revenue per Passenger (2)(3) 1. Includes ancillary and other revenue per passenger. 2. Includes seats, baggage and other ancillary air revenue. 3. $42.89 is 2021 ancillary revenue per passenger. $16 is a passenger interface fee that went into effect April 2022 and is bas ed upon an estimate of the average passenger interface fee charged via suncoutry.com and third - party purchase options. $58.89 assumes the passenger interface fee w as in effect for full year 2021. 4. There can be no assurance that projections or estimates of future performance will be realized. $42.89 $16.00 $58.89 $58.33 $57.65 $56.86 $21.70 $33.14 $40.53 $42.89 2018 2019 2020 2021 • Allows airline to lower base ticket fares which stimulates passenger growth • Stickier than base ticket fares – ancillary revenue does not traditionally decline in weak demand environments • Easier to grow than base ticket fares • Passengers only pay for what they want Ancillary revenue per passenger has grown rapidly and Sun Country is now the industry leader (4)

Differentiated, Leading Charter Business 17 Overview NCAA and professional sports, casino/VIP, US military, among other customers Source: Diio Mi, DOT T - 100. 1. Based on year - end October 2021 passenger block hours. 2. Includes airlines that provide less than 10%. 2014 Domestic Narrowbody Charter Block Hours 2021 Domestic Narrowbody Charter Block Hours (1) • High growth and high margin market leader in narrow - body charter market • Only U.S. scheduled passenger airline with a meaningful charter business • Scheduled seamlessly with passenger business • Contract based business provides recurring revenues • Pass through fuel costs in Q1 resulted in a 12% reduction in effective fuel price per gallon 29% 19% 13% 10% 29% Other 29% 23% 23% 24% Other Charter revenue and block hours are growing following the COVID downturn (2) (2)

More Business Under Charter Contracts 18 Other Select Charter Customers Percentage of Charter Block Hours Under Long Term Contracts (1) 47% 42% 27% 75% 2019 2020 2021 2022E Recent New Customers Details • 5 year agreement to provide charter service to all Major League Soccer teams - Agreement began at the beginning of 2022 • 5 year agreement to provide charter service for Caesars Entertainment guests - Agreement began in March 2022 1. There can be no assurance that projections or estimates of future performance will be realized.

19 Unique, Asset - Light Cargo Business Key Highlights Statistics • 12 Boeing 737 - 800 freighter aircraft operated on behalf of Amazon • Amazon supplies the aircraft, pays for many flight expenses, including fuel and is responsible for all cargo - related activities (including loading / unloading) • 10 year contract, initial term six years and two, two - year extension options • Since contract was signed with Amazon in 2019, all of Amazon’s new 737 cargo aircraft have been assigned to Sun Country x Third largest narrowbody cargo operator in the U.S (1) x High margin and cash flow with stable revenue and pass - through cost structure x Asset light business with no ongoing capex x Synergistic with other business lines, leveraging pilots and other shared resources x Partnership with one of the fastest growing companies globally 11% Variance in Daily Block Hours, Driving Operational Stability $0 Ongoing Capital Expenditures $91mm LTM Q1 2022 Revenue 100% Fuel Costs Paid by Amazon Partnership between Amazon and a scheduled passenger service carrier with stable, high margin revenue and cash flow Overview 1. Based on LTM Q1 2022 block hours.

Ratified Pilot Contract Unlocks Growth 20 Key Benefits • Pay scales and benefits competitive with low - cost peers and on par with current legacy rates by 2025 • First airline to ratify new pilot contract post - COVID, providing predictable costs • Effect has been reduced attrition and increase in applicants • Adds flexibility and unlocks potential future cargo growth • Improves pilot quality of life • Negotiated in less than 4 months – Cooperation between pilots and management 1. There can be no assurance that projections or estimates of future performance will be realized. 2. Adj cost per block hour = GAAP total operating expense – fuel expense – special items, net / total block hours. Despite higher pilot cost starting in 2022, Sun Country’s strong cost control has resulted in 2022E adjusted operating expenses per block hour being 3% lower than in 2019 (1)(2)

Decline in Key Cost Categories Over Time 21 Total Expense Per AC (1) Per Month Distribution Costs per Passenger (2) Source: Public filings. 1. Passenger aircraft only, includes rent, debt service and reserve payments. 2. Includes call center, GDS fees, OTA fees, and credit card fees. $266 $246 $246 $194 2018 2019 2020 2021 $9.78 $8.68 $8.01 $7.69 2018 2019 2020 2021 Mix Indirect Direct 59% 52% 74% 74% 41% 48% 26% 26% ($000) Combined with high fuel pass through, lower ownership costs further enable Sun Country to maintain high margins during high - fuel price environments

Positioned for Continued Growth

Unique Set of Vectors to Propel Growth 23 …and is uniquely positioned to pursue the most advantageous growth opportunities across Scheduled Service, Charter and Cargo Sun Country has multiples levers for growth… • Significant additional MSP growth (same store & new markets) opportunities exist to realize full potential • Operational flexibility unlocks non - MSP growth ▪ Capitalize on seasonal demand spikes; particularly in Q3 • Upper Midwest focus where brand recognition is strong Scheduled Service Charter Cargo • Additional contracted business opportunities in casinos and sports • Return of ad hoc flying as pilot availability constraints ease • Select opportunities for dedicated aircraft, similar to current Kona business • Amazon expected to continue strong growth trends • Sun Country continues to be a high reliability supplier • Opportunity to diversify to freight companies

Scheduled Service Growth Builds On Capabilities 24 Sun Country's Scheduled Service Growth Plan (1) Total ASMs in millions (MSP and non - MSP) 1. There can be no assurance that projections or estimates of future performance will be realized. Non - MSP • Super - scraper: high seasonal peaks in large markets (DFW - CUN) • Upper Midwest: brand extends well, similar seasonalities to MSP • Strong profitability: 2021 margins outperformed MSP • Added 17 new Non - MSP markets in 2021 MSP • Existing markets : ability to continue growth based on share gains in the market (5 core markets) • Significant growth: still have over 80 unserved markets with more than 30 daily passengers from MSP • New market success: grown nonstop markets by over 40% vs. ‘19, nearly all met performance threshold • Added 17 new MSP markets in 2021 5,573 8,374 734 2,631 2022E 2023E 2024E 2025E MSP Non-MSP Sun Country expects to continue to grow based on “playbook” that has demonstrated successes

Sun Country Has Been Growing its Share at MSP 25 Cumulative Change in MSP Passenger Share Since 2017 (1)(2) Source: Diio Mi, DOT O&D. 1. Based on year - end Q3 passengers per day. 2. SNCY – Sun Country, DAL – Delta. Second largest carrier at MSP with significant room to continue taking share from smaller players in the market 0% 1% 4% 6% 2% 3% 1% 3% (2%) (4%) (5%) (9%) (12%) (9%) (6%) (3%) 0% 3% 6% 9% 2017 2018 2019 2020 2021 SNCY DAL Others Current Share 58% 23% 18%

Ancillary Revenue Growth Potential 26 1. Includes ancillary and other revenue per passenger. 2. $16 is a passenger interface fee that went into effect April 2022 and is based upon an estimate of the average passenger inte rfa ce fee charged via suncoutry.com and third - party purchase options. 3. There can be no assurance that projections or estimates of future performance will be realized. • Enhanced Merchandising – improved offer and product presentation on suncountry.com, including bundled ancillary products • New Products – introduction of new product offerings • Pricing Optimization – improved technology enabling enhanced pricing practices, including machine learning • 3rd Party Products – continued expansion and optimization of the 3rd party product portfolio Ancillary Revenue per Passenger Growth Range (1)(3) Initiative Areas $21.70 $33.14 $40.53 $42.89 2018 2019 2020 2021 2024E $2 to $5 per Pax of Ancillary Upside Ancillary revenue per passenger is expected to continue to grow, driven by better merchandising, new products and pricing initiatives Passenger Interface Fee of $16 (2)

Charter Flying Growth 27 Charter Flying (1) 1. There can be no assurance that projections or estimates of future performance will be realized. 2019 2022E Growth Plan 78% 150% 150%+ 100% 2019 charter block hours = 19,852 % of 2019 total block hours Ad hoc charter flying Charter flying under contract Return of ad hoc flying to 2019 levels + fleet growth Represents $20 - $25mm of revenue upside Charter flying under contract has grown by 150% since 2019; return of ad hoc business will drive growth in 2022 and 2023 Growth opportunities exist with current and new customers

Amazon Shipping Requirements to Continue to Grow 28 U.S. Amazon E - Commerce Revenue (1) Historic Amazon Delivery Expenditures Source: BofA Global Research, “Global eCommerce Outlook” 10/13/2021. 1. Includes 3rd party sales, excludes Whole Foods Market. $150 $174 $206 $291 $341 $392 $450 $512 2017 2018 2019 2020 2021 2022 2023 2024 $22 $28 $38 $61 $77 2017 2018 2019 2020 2021 Market Share 34% 34% 36% 38% 41% 41% 41% 41% YoY Change 22% 16% 14% 15% 15% 17% 41% 18% 34% 28% 37% 61% 26% ($bn) ($bn) New pilot contract contains provisions which facilitate additional cargo growth for Sun Country

Responsible Fleet Growth 29 1. As of June 2022. 2. There can be no assurance that projections or estimates of future performance will be realized. With no order book and extensive experience purchasing mid - life aircraft, Sun Country can opportunistically acquire aircraft at lower prices Total Aircraft in Service Strategy in Place to Support Fleet Growth 31 36 42 12 12 12 31 43 48 54 2019 2020 2021 Current 2025E Passenger AC Cargo AC Total 70 - 75 • Restructured fleet with a focus on ownership of Boeing 737 - 800s with low capital commitments • The 737 - 800 is the LCC stalwart for airlines such as Southwest and Ryanair • Sun Country maintains no order book and acquires aircraft based on demand needs • COVID and re - start of 737 Max deliveries has created unique opportunities to acquire mid - life aircraft at favorable prices (# of aircraft) (2) (1)

Balance Sheet Positions Sun Country for Growth 30 Liquidity (1) / TTM Revenue Deleveraging Through the Pandemic & Recovery (Adj. Net Debt / LTM EBITDA (2) ) • $297m of liquidity at first quarter 2022 provides ample capital to support growth • Manageable CAPEX requirements given mid - life passenger fleet; cargo segment asset - lite • No non - aircraft debt • Reduced debt levels during COVID 1. Liquidity is cash balance + undrawn portion of revolver. 2. Net leverage calculated as adj. net debt / EBITDA. Adj. net debt defined as long - term debt, finance leases, operating leases, le ss cash & equivalents. 10% 22% 54% 41% 2019 2020 2021 LTM Q1 2022 2.4x 3.3x LTM Q1 2022 FY 2019

Non - GAAP Reconciliations

Description of Special Items Special Items, Net – in millions USD FY 2018 FY 2019 FY 2020 FY 2021 CARES Act grant recognition $0.0 $0.0 ($62.3) ($71.6) CARES Act employee retention credit - - (2.3) (0.8) Contractual obligations for retired technology - 7.6 - - Sale of airport slot rights - (1.2) - - Sun Country Rewards program modifications (8.5) - - - Early - out payments and other outsourcing expenses 2.0 - - - Aircraft purchases impacts - - - 7.0 Other - 0.7 - - Total Special Items, net ($6.4) $7.1 ($64.6) ($65.5) Numbers may not add due to rounding 32

Non - GAAP Reconciliation – Adj Operating Income Adjusted Operating Income is included as a supplemental disclosure because we believe it is a useful indicator of our operati ng performance. Adjusted Operating Income is a well recognized performance measurement in the airline industry that is frequently used by our management, as wel l a s by investors, securities analysts and other interested parties in comparing the operating performance of companies in our industry. Adjusted Operating Income Reconciliation – in millions USD FY 2019 FY 2020 FY 2021 Q1 2022 Operating Income $78.1 $17.4 $107.0 $21.8 Special items, net (1) - (64.6) (65.5) - Stock compensation expense 1.9 2.1 5.6 0.9 Employee relocation and costs to exit Sun Country’s prior headquarters building and base closures 0.7 - - - Contractual obligations for retired technology 7.6 - - - Sale of airport slot rights (1.2) - - - Tax receivable agreement expense (2) 0.3 - Voluntary leave expense (3) 4.9 - - Other adjustments 0.2 - 3.0 - Adjusted operating income 87.3 (40.2) 50.5 22.8 Total revenue $701.4 $401.5 $623.0 $226.5 Adjusted operating income margin 12.5% (10.0%) 8.1% 10.0% 1. See Description of Special Items table in this Appendix 2. This represents the one - time costs to establish the Tax Receivable Agreement (“TRA”) with our pre - IPO stockholders 3. This includes expenses related to a voluntary employee leave program in response to the COVID - 19 pandemic, a portion of which is offset by the CARES Act Payroll Support Program as the benefit of this program is also adjusted as a component of special items Numbers may not add due to rounding 33

Non - GAAP Reconciliation – Adj EBITDA Adjusted Earnings Before Interest, Taxes, and Depreciation & Amortization (“EBITDA”) is included as a supplemental disclosure be cause we believe it is a useful indicator of our operating performance. Adjusted EBITDA is a well recognized performance measurement in the airline industry tha t is frequently used by our management, as well as by investors, securities analysts and other interested parties in comparing the operating performance of companies in our industry. 1. See Description of Special Items table in this Appendix. 2. Other adjustments for FY 2020 include expenses related to a voluntary employee leave program in response to the COVID - 19 pandemi c, a portion of which is offset by the CARES Act Payroll Support Program as the benefit of this program is also adjusted as a component of special items. Other adjustments for FY 2019 includ e e xpenses incurred in terminating work on a planned new crew base. Other adjustment for represents expenses for secondary stock offering by Apollo and other stockholders and pilot CBA vacation adjus tme nt 3. This represents the one - time costs to establish the Tax Receivable Agreement (“TRA”) with our pre - IPO stockholders 4. This represents the adjustment to the TRA for the period, which is recorded in Non - operating (Income) / Expense Numbers may not add due to rounding Adjusted EBITDA Reconciliation – in millions USD FY 2018 FY 2019 FY 2020 FY 2021 Q1 2022 Q1 2021 LTM Q1 2022 Net income (loss) $25.5 $46.1 ($3.9) $77.5 $3.6 $12.4 $68.7 Provision for income taxes 0.2 14.1 (0.8) 18.0 2.8 5.4 15.4 Interest expense 6.4 17.2 22.1 26.3 8.6 7.1 27.8 Interest income (0.4) (0.9) (0.4) (0.1) - - (0.1) Special items, net (1) (6.4) 7.1 (64.6) (65.5) - (26.9) (38.6) Tax receivable agreement expense (3) - - - 0.3 - 0.3 - Tax receivable agreement adjustment (4) - - - (16.4) 6.8 - (9.6) Stock compensation expense 0.4 1.9 2.1 5.6 0.9 2.9 3.6 Loss (gain) on asset transactions, net (0.8) 0.7 0.4 - - - - Other adjustments (2) - 0.2 4.9 4.8 - - 4.8 Depreciation and amortization 16.9 34.9 48.1 55.0 15.3 12.6 57.7 Adjusted EBITDA 41.8 121.3 7.9 105.5 38.0 13.8 129.7 Adjusted EBITDA margin 7.2% 17.3% 2.0% 16.9% 16.8% 10.8% 18.0% Total revenue $582.4 $701.4 $401.5 $623.0 $226.5 $127.6 721.9 34

Non - GAAP Reconciliation – Adj CASM Adjusted CASM, which is a non - GAAP financial measure, is also a key airline cost metric and excludes fuel costs, costs related t o our freighter operations (starting in 2020 when we launched our freighter operation), certain commissions and other costs of selling our vacations product from thi s m easure as these costs are unrelated to our airline operations and improve comparability to our peers. Adjusted CASM is one of the most important measur es used by management and by our board of directors in assessing quarterly and annual cost performance. Adjusted CASM is also a measure commonly used by indus try analysts and we believe it is an important metric by which they compare our airline to others in the industry, although other airlines may exclude certain oth er costs in their calculation of Adjusted CASM. Adjusted CASM Reconciliation – in millions USD, except for ASMs and Adjusted CASM FY 2017 FY 2018 FY 2019 FY 2020 FY 2021 Q1 2022 Operating expense – as reported $530.0 $549.0 $623.3 $384.1 $516.0 $204.7 Aircraft fuel (118.4) (165.3) (165.7) (83.4) (129.1) (64.5) Cargo expenses, not already adjusted - - - (31.4) (67.2) (19.1) Sun Country Vacations (2.1) (4.5) (2.4) (0.6) (0.8) (0.4) Special items, net (1) - 6.4 (7.1) 64.6 65.5 - Stock compensation expense - (0.4) (1.9) (2.1) (5.6) (0.9) Tax receivable agreement expense (2) - - - - (0.3) - Voluntary leave expense (3) - - - (4.9) - - Other adjustments - - (0.2) - (3.0) - Adjusted operating expense $409.5 $385.2 $445.9 $326.3 $375.4 $119.7 Available seat miles (ASMs) – millions 5,250.5 5,463.2 7,064.6 4,311.1 5,826.8 1,928.1 Adjusted CASM - cents 7.80 7.05 6.31 7.57 6.44 6.21 1. See Description of Special Items table in this Appendix 2. This represents the one - time costs to establish the Tax Receivable Agreement (“TRA”) with our pre - IPO stockholders 3. This includes expenses related to a voluntary employee leave program in response to the COVID - 19 pandemic, a portion of which is offset by the CARES Act Payroll Support Program as the benefit of this program is also adjusted as a component of special items Numbers may not add due to rounding 35

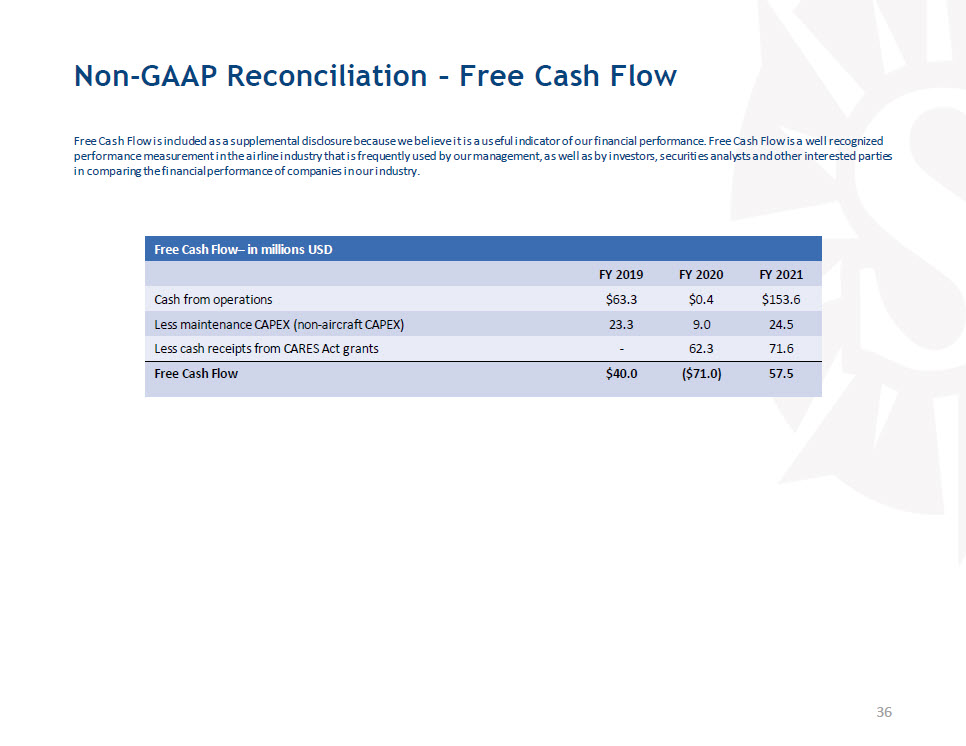

Non - GAAP Reconciliation – Free Cash Flow Free Cash Flow is included as a supplemental disclosure because we believe it is a useful indicator of our financial performa nce . Free Cash Flow is a well recognized performance measurement in the airline industry that is frequently used by our management, as well as by investors, securitie s a nalysts and other interested parties in comparing the financial performance of companies in our industry. 36 Free Cash Flow – in millions USD FY 2019 FY 2020 FY 2021 Cash from operations $63.3 $0.4 $153.6 Less maintenance CAPEX (non - aircraft CAPEX) 23.3 9.0 24.5 Less cash receipts from CARES Act grants - 62.3 71.6 Free Cash Flow $40.0 ($71.0) 57.5